Compound interest is the addition of interest to the principal sum of a loan or deposit. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest. In a nutshell that sentence answers the question ‘what are compound interest rates’. In addition, compound interest can be used to increase savings and earnings as it makes use of all of the money involved in some form, rather than just the original principal. Interest rates have an effect on compound interest rates and can impact overall returns, which should be considered before making any financial decisions involving compound interest and deposit accounts.

How do compound interest rates work?

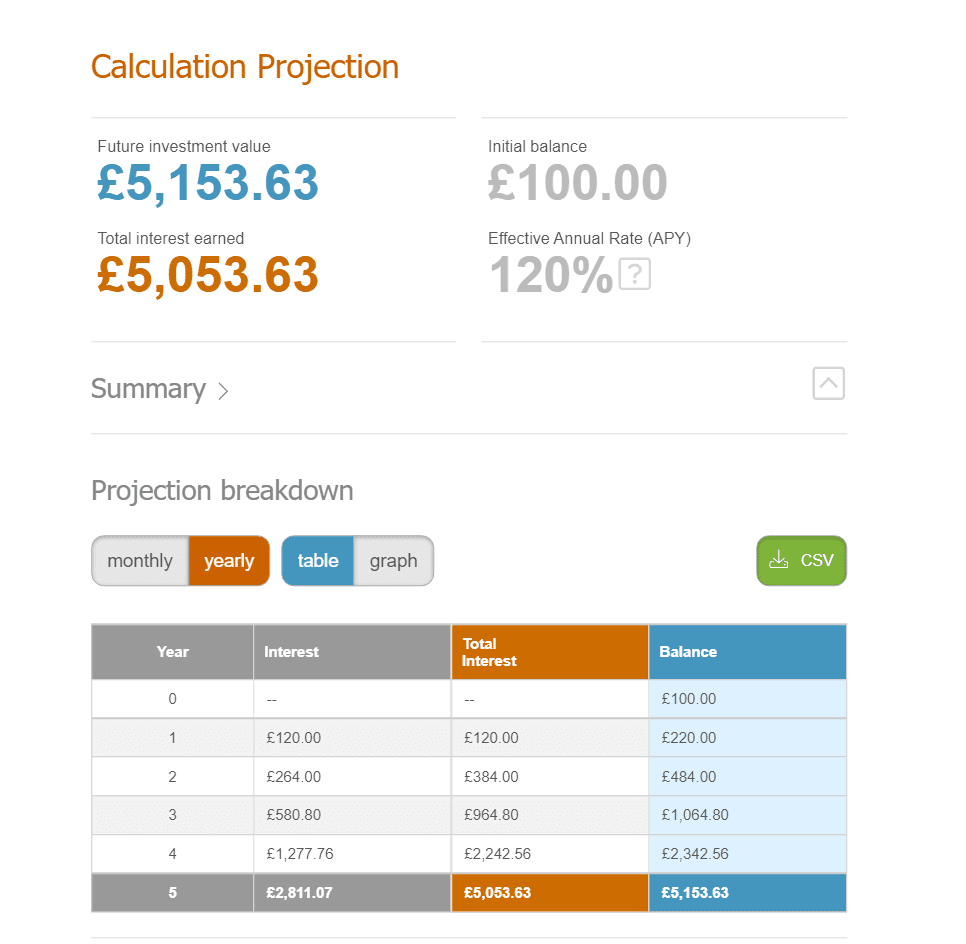

There are two kinds of interest rates you need to know about: compound interest rates and simple interest rates. If a financial institution offers a 10% compound interest rate, that means you earn not only 10% on your initial deposit, but also on any added interest from previous periods. Look at our table here to see the effects of interest being compounded onto your initial £100 investment. It adds up quickly! Thanks to The Calculator Site for use of their calculator.

How much should you be saving?

The higher your interest rate and how much you’re able to save, in theory, the more money you can earn from interest. But do high compound interest rates necessarily mean you’ll be able to save more? For example, compare two different credit cards: one with a 2 percent annual percentage rate (APR) and another with an 18 percent APR. As you might expect, a card with a higher APR will cost more—but there’s something else to consider.

In most cases, cards that charge such high interest rates also have lower limits on their credit lines. This means you won’t be able to put as much of your expenses on those cards as others. Moreover, many issuers calculate a borrower’s credit limit by taking into account his or her debt-to-income ratio. With a low limit on your card—and thus less room for additional debt—the same amount of interest accrued could result in less available cash at month’s end than it would if spread across multiple cards.

On top of that, many providers offer discounts for customers who pay their balance in full each month; why not make every pound count? What might seem like small savings now could add up to hundreds or thousands over time. While compounded interest is beneficial when used properly, it can quickly become dangerous when you let things get out of hand. There are plenty of resources online offering advice on investing wisely; be sure to educate yourself before making any moves toward potential wealth accumulation.

When will you start earning compound interest?

To understand when you’ll start earning compound interest, it’s important to be familiar with some of its basic terminology. The term compounding period refers to how often you earn interest, typically either annually or monthly. For example, if your bank compounds interest on a quarterly basis (i.e., every three months), then your compounding period is three months. Then there’s also principal, which can refer to how much money is initially deposited into an account, or in our case invested. Finally, what most people are actually referring to when they say interest rate—or annual percentage yield—is essentially the compound interest rate. It represents what percent of your investment will grow each year because of reinvestment and compounding.

What are the benefits of compound interest?

One of the major benefits of compound interest is that it allows your investment to earn more money for you. For example, if you put £1,000 into an account at a 1% interest rate that compounds annually, in five years you will have £1,050. If you instead received a flat 1% interest rate each year on your investment and did not re-invest any amount of interest back into your account for those five years, after five years you would only have £1,020. The extra income from compound interest allows your balance to grow substantially over time. In fact, there are many scenarios where a high enough rate of compounded growth can even lead to exponential growth. See our table above (growing faster than inflation). Some forms of investing such as options trading or stock market investments, it has been proven possible on multiple occasions.

Tips for Maximizing Your Compound Interest

It’s important to maximize your compound interest. To do so, you should always invest in vehicles that earn a higher interest rate. For example, let’s say you have £10,000 to invest and opt for a 1% return on your investment. It will take two decades to double your money. Instead, let’s say you choose a 2% return investment with that same initial £10K. This time reinvest all of your interest payments over time and you will double your money in just 10 years! Be sure to make extra principal payments (pay down loans faster) whenever possible.

Whenever an additional payment is due from you on a loan or line of credit, call your lender or service provider and set up an automated recurring payment plan to pay off that loan early. Doing so can give your money more opportunity to grow via compound interest. It will also save yourself thousands in interest charges by paying off debt sooner rather than later.

The importance of consistency

If you want to start saving and investing money at a young age, it’s important to do so consistently. If you can save a little bit each month, you’ll be surprised at how quickly it adds up. It will turn into meaningful amounts of money that could make a big difference in your future. This is one habit that pays off more than you may expect! It can be easy to think, It’s never too early or late to start investing—there’s still time!

Looking for something else? Personal Loans Payday Loans Bad Credit Loans