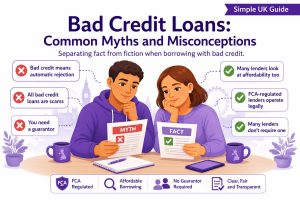

Bad credit does not automatically prevent you from borrowing money.

While your options may be more limited, many UK lenders will consider applications from people with less-than-perfect credit histories. The key question isn’t simply whether you have bad credit but whether you can afford to repay the loan.

These loans can provide a financial solution for those facing challenges due to their credit history.

If you’re considering applying for 2000 loans for bad credit, here’s what you need to know.

Can You Get a £2,000 Loan With Bad Credit?

Yes, it may be possible.

Some lenders specialise in helping people with poor or limited credit histories. Others assess every application individually, looking at your current financial circumstances rather than focusing solely on your past.

A poor credit history may affect:

- The lenders willing to consider your application.

- The interest rate you are offered.

- The repayment period.

- The amount you can borrow.

What Do Lenders Look At?

Modern lenders carry out affordability checks rather than relying on your credit score alone.

They may consider:

- Your income.

- Your employment status.

- Your monthly household expenses.

- Existing credit commitments.

- Your recent repayment history.

- Whether the loan appears affordable.

The aim is to ensure that borrowing is suitable for your circumstances.

What Counts As Bad Credit?

Bad credit can mean many different things.

For example:

- Missed payments.

- Defaults.

- County Court Judgments (CCJs).

- A history of payday loans.

- High levels of existing borrowing.

- Little or no credit history.

Not every lender views these issues in the same way.

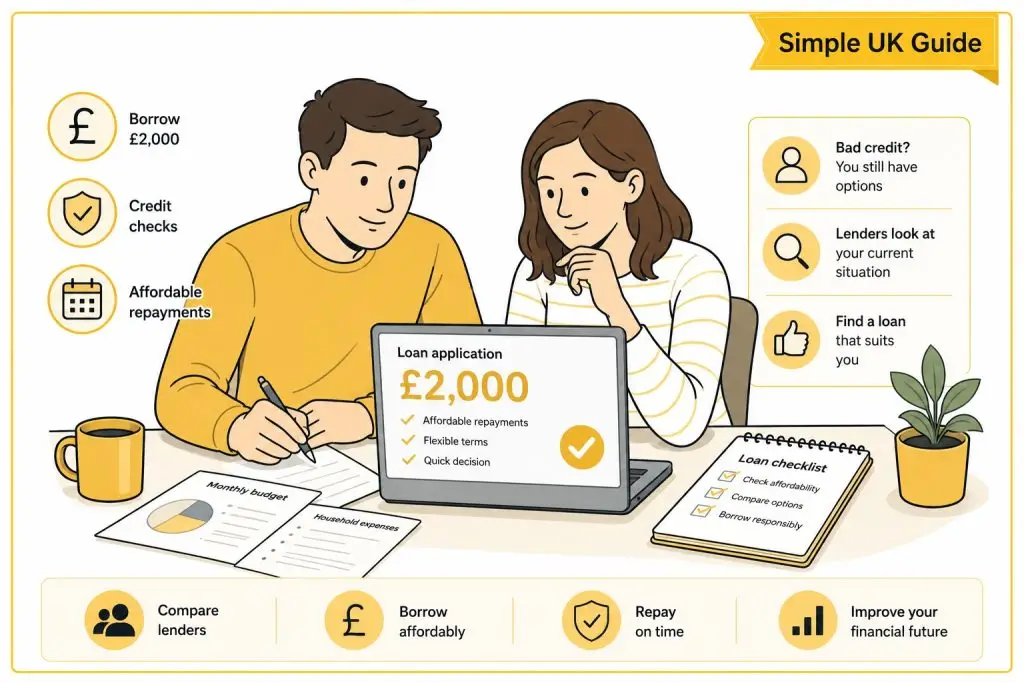

Why Do People Borrow £2,000?

A £2,000 loan is often used for planned or unexpected expenses such as:

- Home improvements.

- Car repairs.

- Debt consolidation.

- Medical or dental treatment.

- Moving home.

- Essential household purchases.

Before applying, think carefully about how much you genuinely need to borrow.

You may find our Loans By Amount page useful if you’re still deciding whether £2,000 is the right amount for your circumstances.

Can You Improve Your Chances?

While no loan is guaranteed, you may improve your chances by:

- Providing accurate information.

- Applying for an affordable amount.

- Ensuring your income and expenditure are realistic.

- Checking your credit file before applying.

- Avoiding multiple applications in a short period.

Honesty and accuracy are always preferable to guessing or exaggerating your circumstances.

Should You Borrow Less?

Sometimes.

If £2,000 is more than you actually need, borrowing a smaller amount could make repayments easier to manage.

For example:

- £500 Loans may suit smaller emergencies.

- £1,000 Loans may be enough for home repairs or moving costs.

Borrowing only what you need can help reduce the overall cost of credit.

Alternatives If You’re Declined

If you’re unable to obtain a £2,000 loan, consider:

- Improving your credit profile before reapplying.

- Saving towards the purchase.

- Reducing the amount you need.

- Looking at other forms of finance where appropriate.

Our Credit Repair service contains practical advice that may help improve your financial profile over time.

Często zadawane pytania

Can I get a £2,000 loan with a poor credit score?

Yes. Some lenders consider applicants with poor credit, although approval is never guaranteed.

Will bad credit stop me borrowing?

Not necessarily. Lenders consider affordability as well as your credit history.

Is a £2,000 loan harder to get than a £500 loan?

It depends on your individual circumstances and whether the repayments are considered affordable.

Does checking eligibility affect my credit score?

Many lenders offer eligibility checks that do not affect your credit score.

Should I apply with several lenders at once?

Generally, no. Multiple applications within a short period may reduce your chances of approval.

Related Pages

- Loans By Amount

- How Much Can I Borrow?

- £2,000 Loans

- £1,000 Loans

- £500 Loans

- What Credit Score Do You Need For a £1,000 Loan?

Useful External Resources

- FCA guidance on creditworthiness and affordability.

- MoneyHelper guide to borrowing money and loans.