Borrowing Isn’t Your Only Choice

If you have bad credit and need money quickly, it can feel like a loan is your only option. However, depending on your circumstances, there may be alternatives that are cheaper, safer or more suitable than taking on additional borrowing.

Under FCA Consumer Duty rules, lenders and credit brokers are expected to act in customers’ best interests. That means considering whether borrowing is genuinely appropriate and helping consumers make informed decisions.

This guide looks at some of the most common alternatives to bad credit loans and explains when they may be worth considering.

Why Consider Alternatives?

A loan can be useful in the right circumstances, but borrowing isn’t always the best solution.

Taking on additional debt may not help if:

- You’re already struggling with existing repayments.

- The financial difficulty is temporary.

- You only need a small amount of money.

- There are cheaper forms of assistance available.

Sometimes a different solution can solve the problem without adding another monthly payment.

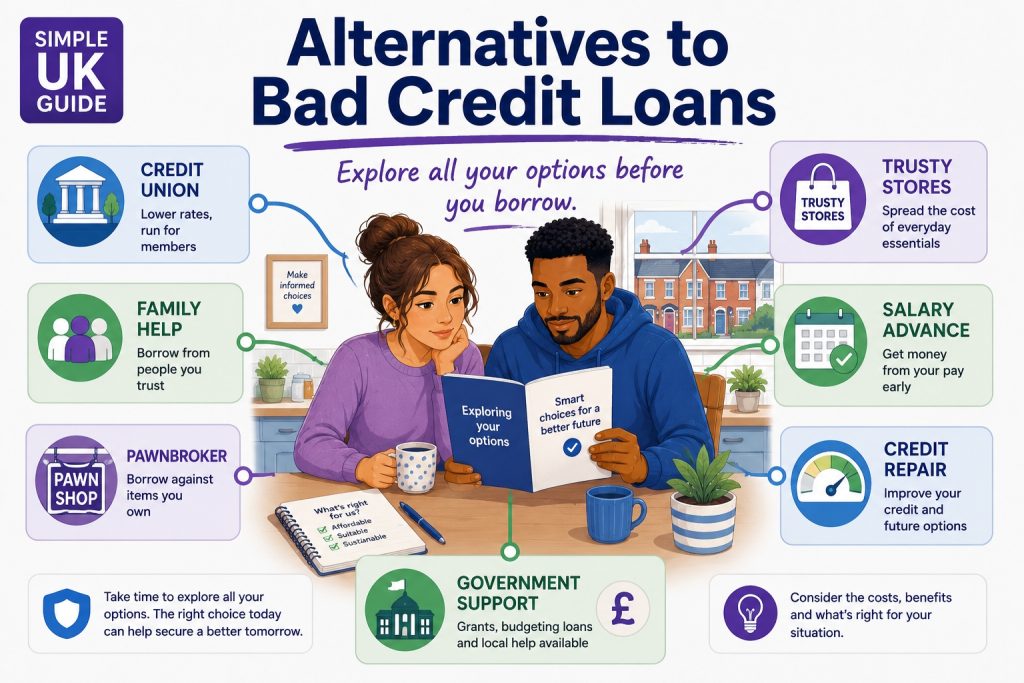

Credit Unions

Credit unions are not-for-profit financial organisations that exist to help their members save and borrow responsibly.

Unlike many commercial lenders, credit unions are focused on supporting their members rather than generating profits for shareholders.

Potential benefits include:

- Lower interest rates.

- More flexible lending decisions.

- Smaller loan amounts.

- Savings facilities.

Credit unions may still carry out credit and affordability checks, but some are prepared to consider applicants who have experienced credit difficulties in the past.

Budgeting Loans and Government Support

Depending on your circumstances, you may be eligible for government assistance.

Some options include:

- Budgeting Loans.

- Budgeting Advances.

- Household Support Fund assistance.

- Local authority grants.

- Discretionary housing payments.

These schemes can sometimes provide help without the need for commercial borrowing.

Family and Friends

Many people dislike asking for help from family or friends. However, it may be one of the cheapest ways to deal with a short-term financial problem.

If you decide to borrow from someone you know:

- Agree repayment terms clearly.

- Put the arrangement in writing.

- Only borrow what you genuinely need.

- Treat the arrangement seriously.

Money can damage relationships when expectations aren’t clear.

Employer Salary Advances

Some employers offer salary advances to employees facing unexpected expenses.

Rather than taking out a loan, you receive part of your wages early and repay the amount through your next payroll cycle.

Potential advantages include:

- No interest charges.

- No credit check.

- Fast access to funds.

- No long-term debt.

Not all employers offer this service, but it is worth asking.

Pawnbrokers

Pawnbrokers have been helping people access short-term funds for centuries.

Instead of relying on your credit history, a pawnbroker lends money against an item of value.

Common items include:

- Gold jewellery.

- Watches.

- Precious metals.

- Collectables.

The loan is secured against the item rather than your credit profile.

If you fail to repay, the pawnbroker may sell the pledged item.

For people who own valuable possessions but have poor credit, pawnbroking can sometimes be a viable alternative.

Selling Unwanted Items

Many households contain items that are rarely used but still have value.

Examples include:

- Mobile phones.

- Tablets.

- Laptops.

- Jewellery.

- Designer goods.

- Tools.

- Collectables.

Selling unwanted possessions may remove the need to borrow altogether.

Trusty Stores and Catalogue Credit

If the money is needed to purchase household goods rather than pay bills, catalogue credit may be worth exploring.

Services such as Trusty Stores can provide access to:

- Furniture.

- White goods.

- Electrical items.

- Household essentials.

For some consumers, spreading the cost of essential purchases may be preferable to taking out a cash loan.

As always, you should understand the costs involved before entering into any credit agreement.

Credit Repair and Credit Building

If borrowing difficulties are being caused by a poor credit history, improving your credit profile may help unlock better options in the future.

Simple steps include:

- Registering on the electoral roll.

- Making payments on time.

- Reducing existing balances.

- Checking credit reports for errors.

- Avoiding multiple loan applications.

Improving your credit score won’t happen overnight, but even small improvements can increase your borrowing options.

Debt Advice Services

If you’re struggling with multiple debts, another loan may not be the answer.

Free debt advice organisations can help you understand your options.

They may be able to assist with:

- Budgeting.

- Debt management plans.

- Negotiating with creditors.

- Understanding your rights.

Seeking advice early often provides more options than waiting until the situation becomes critical.

Emergency Assistance and Charitable Support

Many local councils and charities offer emergency assistance for people facing genuine hardship.

Support may include:

- Food vouchers.

- Energy assistance.

- Essential household goods.

- Crisis grants.

These schemes are often overlooked but can provide valuable short-term support.

Consumer Duty and Responsible Borrowing

The FCA’s Consumer Duty requires firms to act in good faith and help consumers achieve positive outcomes.

This means responsible lenders should not simply encourage borrowing when another option may be more suitable.

A good lender or broker should help you understand:

- The true cost of borrowing.

- The risks involved.

- Whether a loan is appropriate.

- What alternatives may exist.

Understanding all your options helps you make better financial decisions.

Końcowe przemyślenia

Bad credit loans can help in certain situations but they are not always the best solution.

Before applying, take a moment to consider whether a credit union, salary advance, government support scheme, catalogue credit, pawnbroker, family assistance or credit repair strategy could achieve the same goal with less risk and lower cost.

The best financial decision is not always the one that involves borrowing.

Ready to see what you could qualify for?

Check your eligibility on our Bad Credit Loans page. Our initial search uses a soft search, so it won’t affect your credit score.

Często zadawane pytania

What is the best alternative to a bad credit loan?

It depends on your circumstances. Credit unions, salary advances, government support and family assistance are often worth exploring before taking on new borrowing.

Can I get help if I’m on benefits?

Possibly. Budgeting Loans, Budgeting Advances and local authority support schemes may be available depending on your circumstances.

Are credit unions safer than payday lenders?

Credit unions are FCA-regulated and operate on a not-for-profit basis. Many people find them a more affordable borrowing option.

Can I borrow money without a credit check?

Most lenders perform some form of affordability assessment. Alternatives such as salary advances or borrowing from family may not involve traditional credit checks.

Is pawnbroking better than a bad credit loan?

For some people it can be. Pawnbrokers lend against an item of value rather than relying on your credit history.

Can Trusty Stores help if I need furniture or appliances?

Trusty Stores may be an option if you need household goods and want to spread the cost rather than taking out a cash loan.

Will improving my credit score give me more borrowing options?

Yes. Better credit often leads to more lenders, lower interest rates and improved approval chances.

Should I take out another loan to repay existing debt?

Not always. Free debt advice should be considered before taking on additional borrowing.

What does Consumer Duty mean for borrowers?

Consumer Duty requires FCA-regulated firms to act in customers’ best interests and support good financial outcomes.

Where can I get free debt advice?

Organisations such as StepChange Debt Charity and National Debtline provide free assistance.

Related Guides

If you’re researching bad credit borrowing, these guides may also help: