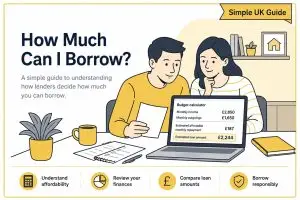

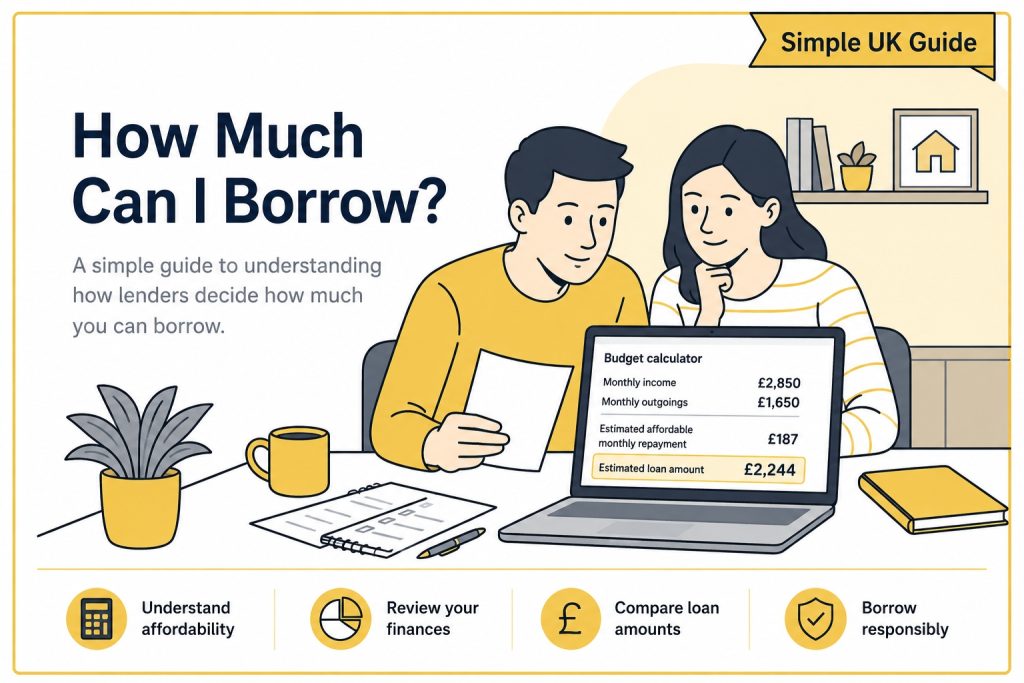

One of the most common questions people ask before applying for a loan is, “How much can I borrow?”

The answer depends on several factors, including your income, existing financial commitments, credit history and the lender’s affordability assessment.

While it can be tempting to apply for the maximum amount available, borrowing only what you genuinely need is often the most sensible approach.

How Do Lenders Decide How Much You Can Borrow?

Every lender has its own criteria, but most will consider:

- Your income

- Your employment status

- Your monthly outgoings

- Existing loans and credit commitments

- Your credit history

- Whether the repayments are affordable

Modern lending decisions focus heavily on affordability rather than simply your credit score.

This helps lenders determine whether you can comfortably repay the loan without experiencing financial difficulties.

Why Income Matters

Your income is usually one of the biggest factors in determining how much you may be able to borrow.

Someone earning £40,000 per year will generally have access to higher borrowing amounts than someone earning £20,000 per year, assuming their financial commitments are similar.

Lenders will often ask for details about:

- Salary

- Benefits

- Self-employed income

- Pension income

- Other regular income sources

The more stable your income appears, the more confidence a lender may have in your ability to repay.

Existing Financial Commitments

Lenders also look closely at your existing commitments.

These may include:

- Credit cards

- Personal loans

- Car finance

- Mortgages

- Rent payments

- Child maintenance

- Utility bills

A high level of existing borrowing may reduce the amount a lender is willing to offer.

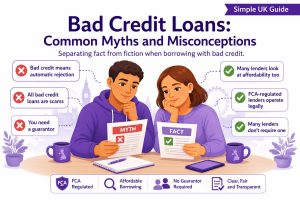

Does Your Credit Score Affect How Much You Can Borrow?

Yes, although not always in the way people expect.

A strong credit history may improve the number of lenders willing to consider your application.

A poor credit history does not automatically prevent you from borrowing, but it may affect:

- The amount available

- The interest rate offered

- The lenders willing to consider your application

You may find our Credit Repair section helpful if you’re looking to improve your credit profile before applying.

Not sure which loan amount is right for you? Our Loans By Amount page compares popular borrowing amounts, explains what they’re commonly used for and helps you decide whether a £500, £1,000 or £2,000 loan could be more suitable for your needs.

Common Loan Amounts

The amount you need will depend on your circumstances.

£500 Loans

A £500 loan may be suitable for:

- Emergency expenses

- Essential household purchases

- Car repairs

- Unexpected bills

Read our £500 Loans guide to learn more.

£1000 Loans

A £1000 loan may be suitable for:

- Home improvements

- Moving costs

- Family emergencies

- Larger essential purchases

Read our £1000 Loans guide for more information.

£2000 Loans

A £2000 loan may be suitable for:

- Debt consolidation

- Major repairs

- Home improvements

- Larger planned expenses

Read our £2000 Loans guide to learn more.

Should You Borrow the Maximum Available?

Not necessarily.

Many people focus on how much they can borrow when they should really focus on how much they can comfortably repay.

Before applying, ask yourself:

- Do I really need this amount?

- Can I comfortably afford the repayments?

- Would borrowing less achieve the same goal?

- What happens if my circumstances change?

Responsible borrowing is about affordability, not simply accessing the largest loan available.

Alternatives to Borrowing More

Before increasing the amount you borrow, consider whether you could:

- Delay the purchase

- Reduce the amount needed

- Use savings

- Spread costs differently

- Improve your credit profile before applying

Sometimes a smaller loan can achieve the same objective while reducing overall borrowing costs.

ਅਕਸਰ ਪੁੱਛੇ ਜਾਣ ਵਾਲੇ ਸਵਾਲ

ਮੈਂ ਵੱਧ ਤੋਂ ਵੱਧ ਕਿੰਨੀ ਰਕਮ ਉਧਾਰ ਲੈ ਸਕਦਾ ਹਾਂ?

The amount available depends on your income, affordability and the lender’s criteria.

ਕੀ ਮੈਨੂੰ ਮਾੜੇ ਕ੍ਰੈਡਿਟ ਨਾਲ ਕਰਜ਼ਾ ਮਿਲ ਸਕਦਾ ਹੈ?

Many lenders consider applicants with poor credit histories, although the options available may differ.

Does checking eligibility affect my credit score?

Many lenders now offer eligibility checks that do not affect your credit score.

Is it easier to get a smaller loan?

Not always. Affordability and lender criteria remain the key factors.

Should I borrow more than I need?

Generally, borrowing only what you genuinely need is the most sensible approach.

Related Guides

- Can I Get a £2000 Loan With Bad Credit?

- What Credit Score Do You Need For a £1000 Loan?

- £500 vs £1000 vs £2000 Loans: Which Is Right For You?